Charitable Contributions Subject To 10 Floor

March 2019 Charitable Contributions Are They Still Tax Deductible Marin Financial Advisors

The Charitable Contributions Deduction Mercatus Center

The Tax Break Down Charitable Deduction Committee For A Responsible Federal Budget

Pin By Morgan Jackson On Procurement And Sponsorship Lake Oconee Charitable Donations Public Service

Covid 19 And Charitable Contributions By Individuals And Businesses The Cpa Journal

Https Fas Org Sgp Crs Misc If11022 Pdf

Unreimbursed employee expenses subject to the 2 of agi limitation.

Charitable contributions subject to 10 floor.

Pin By Morgan Jackson On Procurement And Sponsorship Lake Oconee Charitable Donations Public Service

Acceptance Package College Acceptance Acceptance College

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Wsj Tax Guide 2019 Charitable Donation Deduction Wsj

Typically Building A House Takes Months Yet A San Franciso Based Company Managed To Build One In Just 24 Hours Located In 3d Printed House 3d Printing House

Prepping Consigned Items For The Sales Floor Flooring Sale Resale Shops Sale

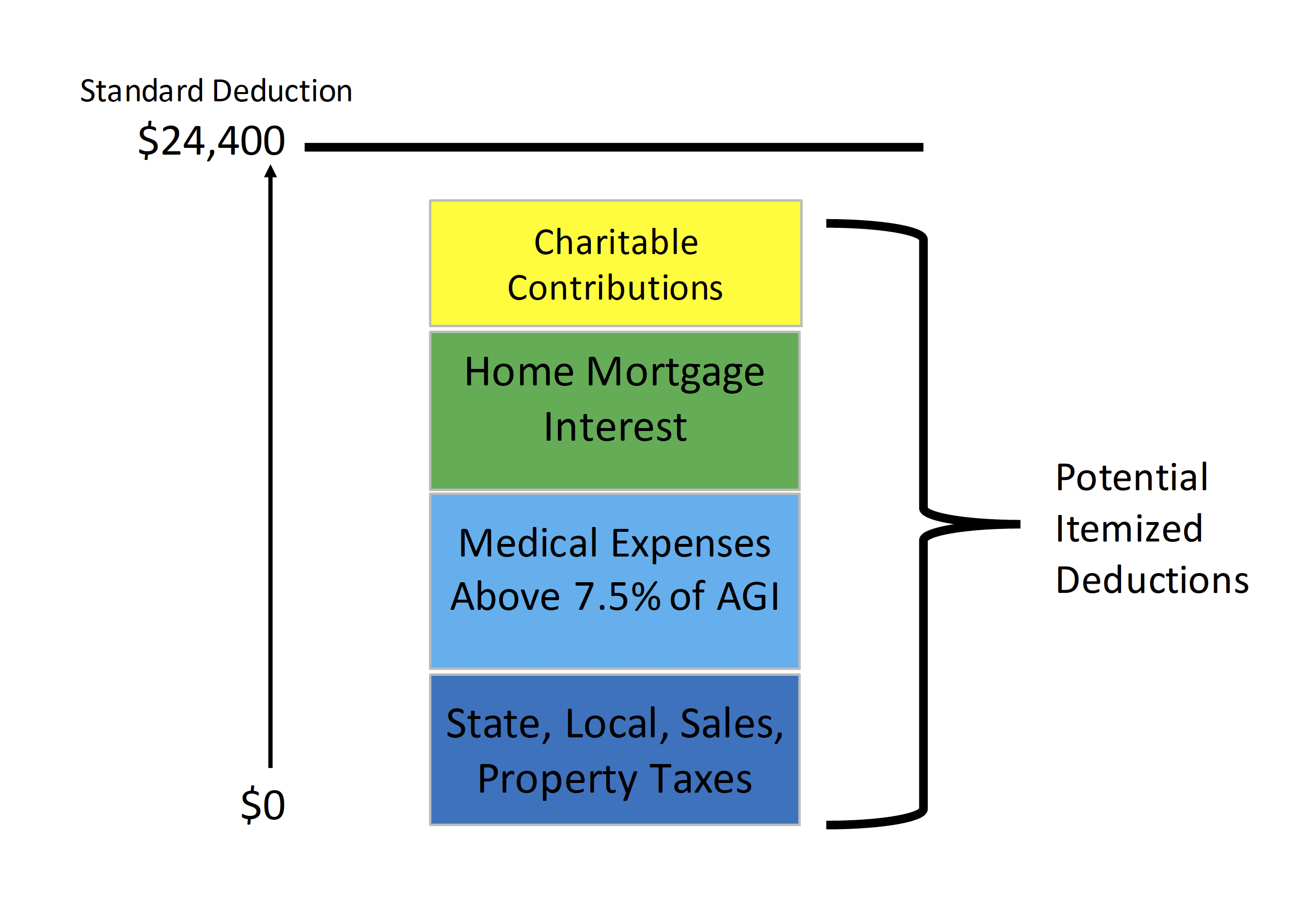

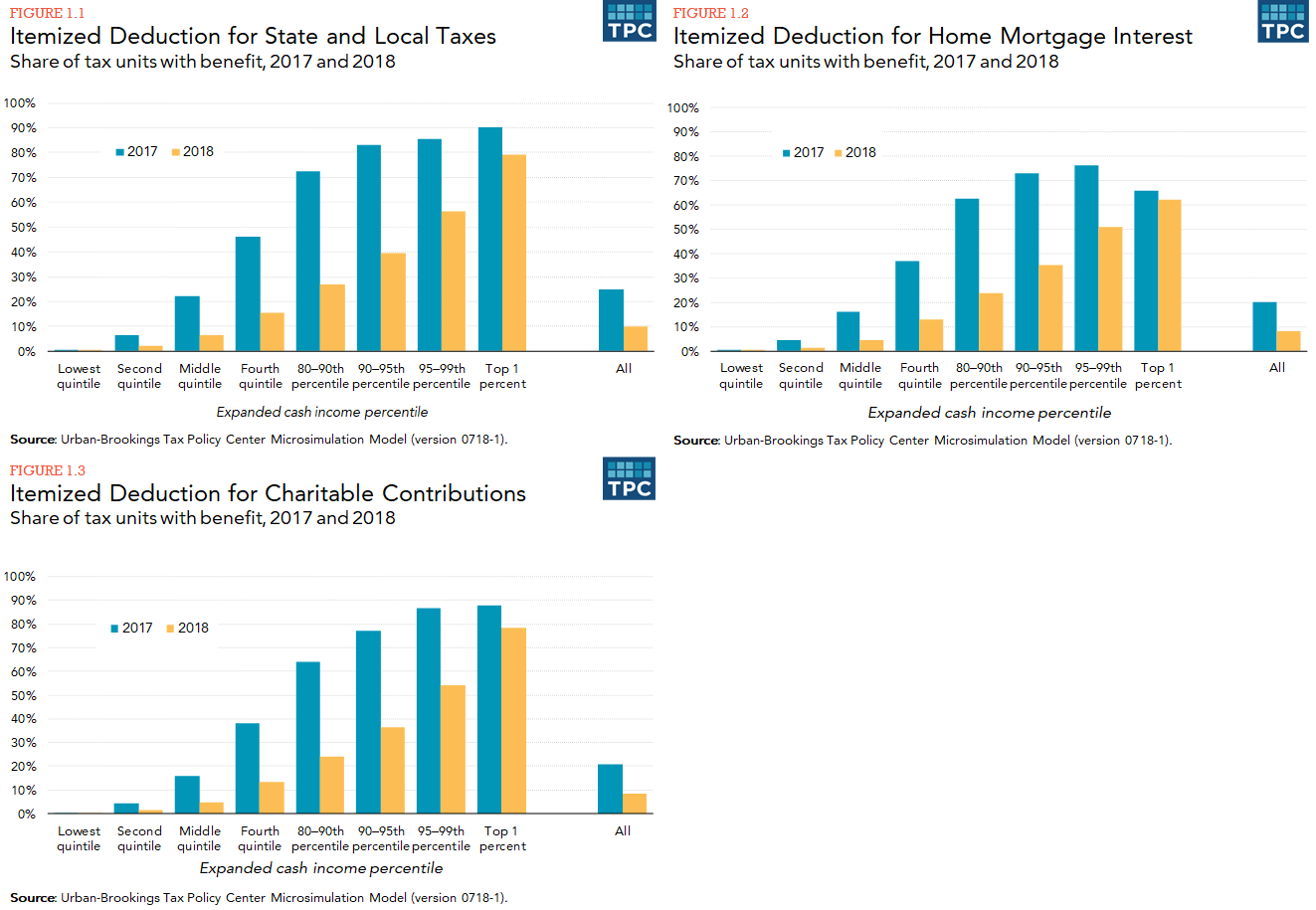

How Did The Tcja Change The Standard Deduction And Itemized Deductions Tax Policy Center

Cares Act Summary Of Tax Provision Blogs Coronavirus Resource Center Back To Business Foley Lardner Llp

43 Ideas Office Decor For Cubicle Professional Must Popular 2019 In 2020 Home Improvement Projects Home Improvement Home Business

10 Most Charitable Celebrities From The 2012 Oscar Nominees Paris Movie Paris Poster Movies

Eastern Connecticut State University Offers A Variety Of Intramural Sports To Participate In The Intramural Sport Intramurals Softball League Women Volleyball

Thompson S Transformation Grid Analysis For The Transition From The Eocene Hyracotherium Skull Form A To The Mo With Images Linear Interpolation Paleontology Mathematics

Funeral Etiquette Funeral Planning Funeral Etiquette Funeral Checklist

Not Every Charitable Donation Is Tax Deductible Gordon Fischer Law Firm

Sanitizing Footbath Floor Mat 24 In 2020 Flooring Floor Mats Cool Inventions

15 Crazy Places For Logos At Events Bizbash Event Event Ideas Creative Corporate Events

Ken Taylor Cheerwine Avett Brothers

Donating Real Estate To Charity What To Know Bader Martin

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctyqeirbje Qet1or2nq Atawapv Ahcg0s7mkn1eolrxxxs434 Usqp Cau

Https Www Jct Gov Publications Html Func Startdown Id 4506

Subtraction Tricks Teaching Math Math Classroom Homeschool Math

Leaping Forward The What And Why Of Edge Computing Edge Computing Is Proving Itself To Be A Durable Conversation Starter Among A Particular Set So It S

Plastolux Keep It Modern Commercial Design Design Workplace Design

Volunteer Thank You Letter Samples Unique Volunteer Appreciation Letter Sample In 2020 Reference Letter Appreciation Letter Reference Letter Template

Source : pinterest.com